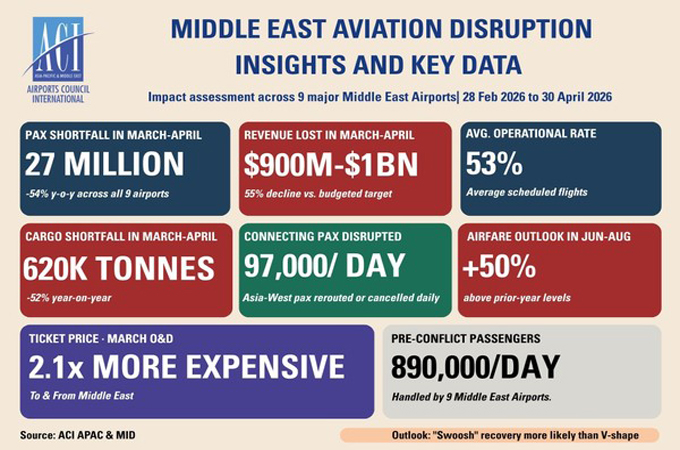

The ongoing conflict in the Middle East has resulted in an estimated $900 million to $1 billion revenue loss for nine major Middle East airports over a two-month period, according to an assessment by Airports Council International Asia-Pacific & Middle East (ACI APAC & MID) in partnership with Flare Aviation Consulting.

This represents a 55% shortfall against a budgeted $1.3–1.4

billion in expected revenues, driven primarily by steep declines in passenger

and cargo traffic and placing significant cash flow pressure on airport

operators with high fixed-cost infrastructure commitments.

Passenger traffic across the nine airports fell by an

estimated 27 million travellers during March and April 2026, marking a 54%

year-on-year decline, according to the report.

The sharpest impact was recorded in March, when 14 million

passengers were lost (down 57%), followed by a further 13 million decline in

April (down 50%).

In 2025, the same

airports handled around 324 million passengers, underscoring their critical

role in global connectivity between Europe, Asia, Africa and the Americas, and

highlighting the scale of disruption across major international transit

corridors.

The assessment, covering the period from the onset of the

conflict through 30 April 2026, found that the nine airports operated at an

average of just 53% of pre-conflict scheduled flight capacity, falling as low

as 32% on the first day before recovering to around 63% by late April.

The disruption also removed nearly one-fifth of global

East–West connecting capacity, affecting roughly 97,000 daily transit

passengers who typically move through Middle Eastern hubs.

Cargo operations were similarly affected, with volumes falling 52% year-on-year to 571,000 tonnes, compared with 1.19 million tonnes in the same period of 2025.

March saw the steepest decline at 59%, while April showed partial recovery but remained 43% below prior-year levels, revealed the report.

The report also highlighted significant increases in

airfares on Asia–West routes, where prices more than doubled in March and

remained around 50% higher by mid-year due to reduced competition and

constrained capacity.

Meanwhile, airport charges remained unchanged due to

regulatory frameworks, despite growing pressure on aviation economics.

It noted that Asia-Pacific traffic trends remained broadly

resilient, though routes to the Middle East saw declines.

A survey of 28 airport operators found that rising jet fuel

prices—rather than supply shortages—are the key operational challenge, with

prices nearly double pre-conflict levels. Airports and governments have been

urged to strengthen fuel security and contingency planning as conditions remain

volatile.

Stefano Baronci, Director General, ACI Asia-Pacific &

Middle East, said: “Middle Eastern hubs are not only regional assets but

essential nodes in the global aviation system. The scale of disruption observed

over two months underscores the critical role of airports as enablers of

connectivity, socio-economic growth, and passenger experience. The aviation

ecosystem in Asia-Pacific and Middle East is proving to be resilient, but we

are at a critical juncture, since a protracted instability over the summer period

may have far more negative impact of the economic sustainability of the airport

sector. Against a backdrop of renewed upward pressure on jet fuel prices,

longer routings driven by geopolitical tensions, persistent supply bottlenecks,

and chronically elevated inflation, public policy should not add yet another

layer of cost to air travel. Further increases in government-imposed levy's,

such as the latest passenger movement charges to passengers departing

Australia, directly undermine connectivity, tourism, trade and consumer

welfare.”

The outlook points to a gradual, “swoosh-shaped” recovery,

dependent on airspace normalisation, fuel stabilisation, and network rebuilding

by carriers. -TradeArabia News Service